Click Here for a Printer Friendly Version

U.S. stocks have outperformed foreign stocks for 15 consecutive years (2010-2024). However, the streak may be coming to an end.

International equities dramatically outhustled domestic counterparts in the first half of 2025. Some of the catalysts included ongoing tariff/trade negotiation, attractive pricing on a relative basis, as well as the slumping U.S. dollar.

Are there other factors at work? Perhaps. Investors may be looking to diversify more than they have in the past.

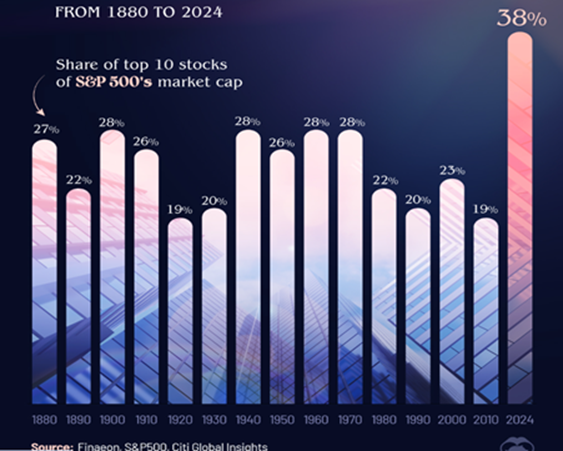

Consider the fact that 10 U.S. stocks account for a larger percentage of the U.S. market than at any other time in recorded history. A whopping 38 percent of the S&P 500 Index’s price movement is attributable to these mega-corporations.

You know their names. Microsoft, Nvidia, Apple, Amazon. The list also includes Meta, Alphabet and Broadcom. Rounding out the top 10 are Tesla, Berkshire Hathaway and J.P. Morgan Chase.

All of them are phenomenal businesses. Over the last decade and a half, their share prices have smashed through a trillion-dollar ceiling that few would have predicted.

On the other hand, stateside portfolios may be concentrated too heavily in the U.S.-based giants. Should the dollar continue to lose value against world currencies, foreign company shares may outperform U.S. stock shares for six years rather than six months.

It has happened before. The U.S. dollar struggled mightily in the first decade of the 21st century. Correspondingly, international equities outshined U.S. equities by a wide margin from 2002-2008. (See the dollar depreciation in the blue box below.)

Here in 2025, the U.S. dollar has already lost 10% of its value, largely due to trade policy uncertainty. The question going forward is whether the world’s reserve currency will drop substantially from here or stabilize at current levels.

In truth, the potential for the dollar to fall further exists. For starters, the Federal Reserve is likely to cut its overnight lending rate two or three times in the months ahead. Rate-cutting activity to stimulate a local economy often weakens a country’s currency.

Global capital may also flow out of U.S. assets, particularly if trade tensions worsen. Furthermore, should the U.S. economy falter in the second half of the year, the dollar downtrend could become entrenched.

What areas tend to perform better or lose less in a weak dollar environment? Multinational companies that generate half or more of their earnings abroad benefit from a weaker dollar. Gold as well as other precious metals tend to surge. Most notably, international investments and emerging economies can shoot up when foreign currencies are trouncing the dollar.

Of course, the U.S. economy may be far more resilient than the financial media portray. For one thing, the Fed expressed that employment is stable and that economic growth is “solid.” And while board members of the Fed’s Open Market Committee (FOMC) still express unease regarding the potential for inflation to pick up, the concern has not materialized.

Still, a crucial ambiguity remains for the investment community: the 90-day tariff pause. If the “ceasefire” does not yield meaningful trade deals, and/or if the pause is not extended further, financial markets are likely to sell off on the lack of clarity.

Today, the Federal Reserve held interest rates steady. However, the central bank of the United States left the door open to multiple rate cuts soon, if inflation remains benign.

Regarding portfolio positioning at Pacific Park Financial, technical indicators support the notion that a long-term stock uptrend is present. Most notably, the monthly closing price for the S&P 500 sits above its 10-month moving average, while the moving average itself is ascending higher. (See the purple arrow and the blue trendline below.)

The current “green-is-for-go” signal reminds us that some warnings do not result in devastating stock bears. The tariff tantrum of April persuaded leaders to rethink a reciprocal tariff approach, ultimately resulting in a 90-day détente to allow for negotiated trade agreements to emerge. This allowed stocks to bounce back quickly in May.

In sum, both U.S. stocks and foreign stocks are trending upward. Foreign stocks represent better “bargains” on traditional valuation measures, and they may continue to profit from U.S. dollar vulnerability.

Granted, U.S. stocks may be pricey, yet they still have widespread appeal for investors worldwide. The same may be said for U.S. bonds; that is, rate hikes are not on the table, while rate cuts are a distinct possibility. Indeed, lower interest rate yields translate to capital gains for bond prices.

Please give us a call or send us an e-mail if you wish to review your portfolio particulars. Similarly, if you would like to discuss the Pacific Park discipline in greater detail, Rob and I are happy to explain how we grow and protect your portfolio.

Warmest Regards,

Gary Gordon, MS, CFP

President