Click Here for a Printer Friendly Version

Blinking is a universal trait. Everybody blinks.

Granted, human beings cannot stop themselves from blinking for long. 30 seconds? One minute? Yet people eventually give into the urge.

The same can be said about trade wars. If a country finds its economy deteriorating rapidly, or watches its financial markets falling precipitously, someone is going to blink. A person, or group of powerful people, will reverse course to quash the damage.

Consider the administration’s tariff rollout. The U.S. stock market’s S&P 500 plummeted nearly 20% from a mid-February high to an early April low. Equally troubling, worldwide investors began selling U.S. Treasury bonds, pushing yields and corresponding borrowing costs dramatically higher. Shortly thereafter, President Trump announced a 90-day pause on its April 2nd tariff launch.

In truth, the 90-day reprieve represented something greater than a pause. It represented a narrative shift from tariff penalty to trade negotiation. Indeed, the shift in focus led to a remarkable recovery for U.S. stocks.

Did the administration need to pivot? Absolutely. Stocks, bonds, and the U.S. dollar were faltering. Global trade was fracturing. Worse yet, lenders had stopped lending.

Even if the administration had chosen to wait, the central bank of the United States, the Federal Reserve or “Fed,” would have blinked. The Fed would have scrambled to avert a recession by slashing interest rates. Board members of the Federal Reserve Open Market Committee (FOMC) might even have voted to print dollars electronically to revive economic activity.

The pivot from trade war to trade negotiation removed the need for the Fed to intervene. What’s more, countries and regions around the globe are eager for business to kick back into a higher gear. It follows that everyone, everywhere, is motivated to negotiate trade deals in good faith.

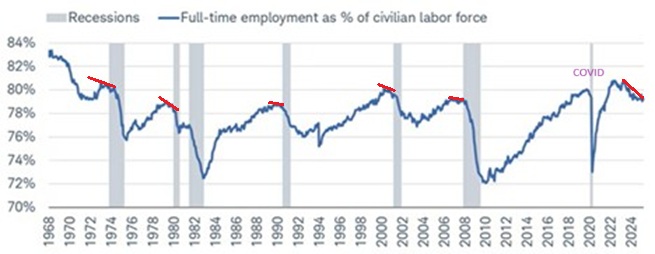

Keep in mind, the U.S. economy and its financial markets are not out of the woods. The retreat of full-time employment could be a sign of recessionary pressure.

There are other “hot spots” as well.

Commercial real estate continues to struggle. Despite numerous employers pushing to get workers back in the office, some may never return for the proverbial five-day work week. The result? Companies no longer require the same square footage. Many businesses are moving to smaller spaces, leaving behind office buildings that they cannot sell.

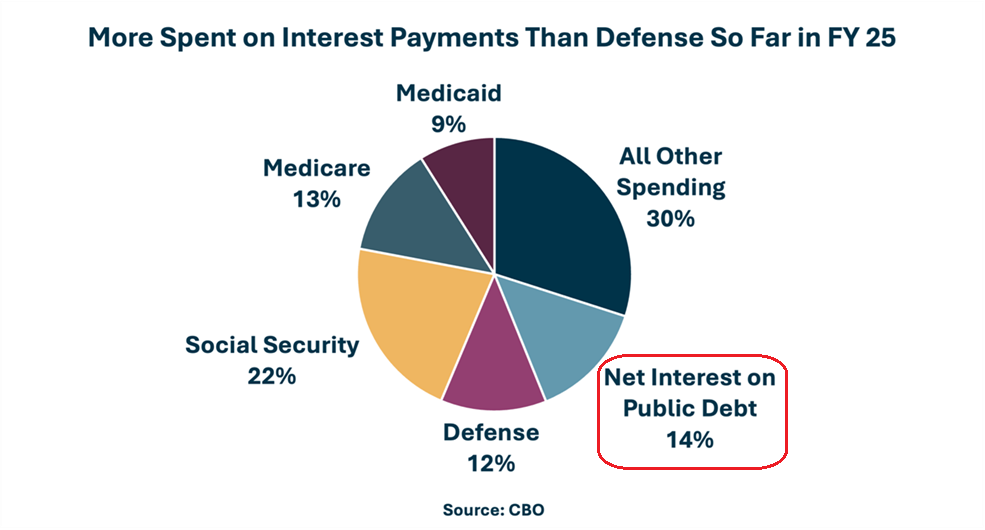

Another flashpoint? Our country’s $36 trillion debt. Congressional spending has become so egregious that, last week, Moody’s lowered the U.S. government’s credit rating. Granted, this is not the first time that a ratings agency has downgraded U.S. sovereign debt. Nevertheless, the lower rating could make it more difficult for Congress to agree on a tax cut package let alone spending restraint.

Despite ongoing economic challenges, the worst-case scenario for a full-blown trade war is behind us. Technical indicators for stocks have improved as well. Over the next few weeks, then, we will restore stock exposure to target levels.

It is worth noting that we intend to take advantage of recent developments. For instance, foreign stocks have been underachievers for more than a decade. Over the last six months, though, foreign stocks have outpaced their U.S. counterparts. Diversifying globally is likely to be very beneficial.

Please give us a buzz or send us an e-mail If you would like to discuss the specifics of your accounts.

Warmest Regards,

Gary Gordon, MS, CFP

President