Do Headlines Help or Hurt Investors?

Click Here for a Printer Friendly Version

Every day, the financial media bombard us with things to worry about. Consumer goods inflation. Higher-for-longer interest rates. Trade policy uncertainty. Decelerating economic growth. The weakening of the U.S. dollar. And an ever-ballooning national debt.

Yet, large company U.S. stocks continue their impressive climb upward. The S&P 500 picked up more than 5% in the first six months of the year and gained additional ground in July.

Not surprisingly, many wonder why the investment markets are ignoring concerns that are supposed to matter. Is it because things are not quite as bad as they are portrayed?

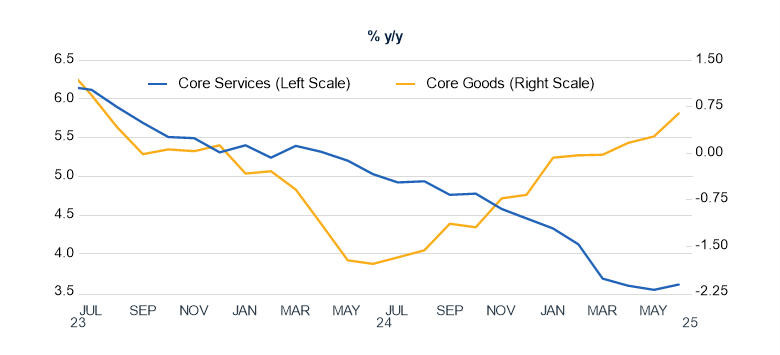

For instance, most financial outlets identified an increase in the Consumer Price Index (CPI). Year-over-year inflation picked up from 2.6% in June to 2.7% in July. What’s more, it has risen from an April low of 2.3%.

Sounds ominous, right? It may be sensible to dig deeper.

For one thing, inflation is down from 3.0% since the start of 2025. Also, services inflation is declining, even as goods inflation heats up.

What this should tell you is that the financial media favor shock-n-awe headline grabbers. Disciplined investors, on the other hand, see greater nuance in the data.

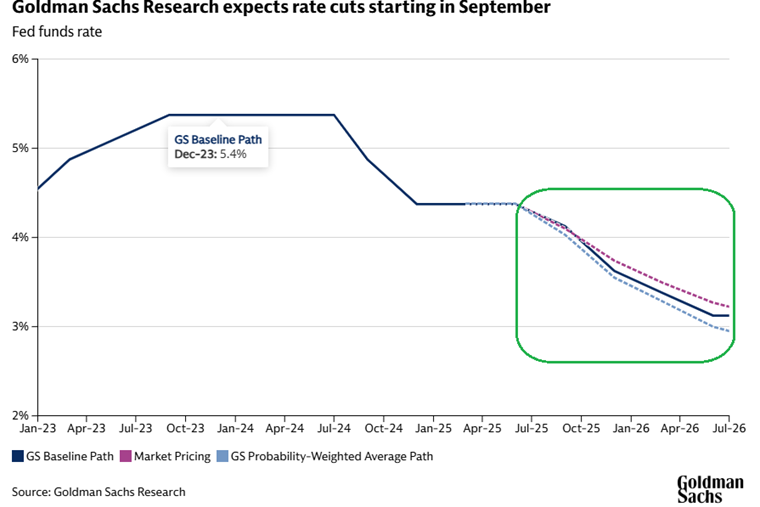

Are there other examples? Absolutely. Look at the commentary on interest rate policy.

Newscasters tend to focus on the Fed’s “wait-n-see” approach to rate cuts, highlighting how the adverse impact of tariffs precludes the prospect of lowering rates this July. Some reporters even point out the possibility that borrowing costs will remain elevated through the end of the year.

The investment community, however, may be looking at a wider range of factors. Reasons to begin dropping rates within a month or two include a moribund real estate environment, a sagging labor market, a decelerating economy, as well as a need to pay less interest on the national debt.

Indeed, the Fed may find itself slashing the cost to borrow money sooner rather than later. There is even a possibility that the White House seeks to replace Fed Chair Powell with a rate-cut-friendly advocate.

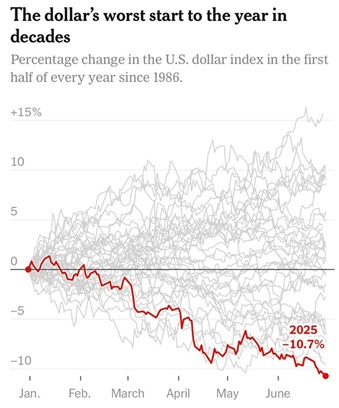

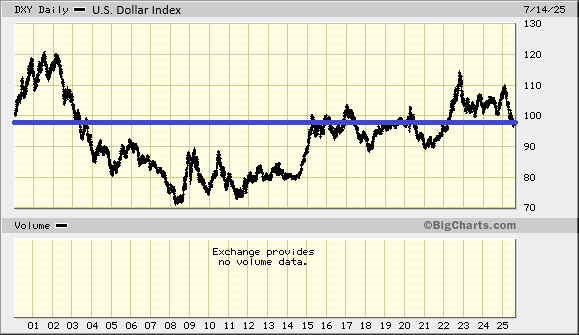

Still another topic that receives a fair bit of press is the dollar’s deterioration.

Many financial journalists are talking about the dollar as if its collapse is imminent. Why? It is down more than 10% since the start of 2025.

However, there are several issues with focusing on a six-month change alone. First, a broader perspective that incorporates the entirety of the 21st century shows the dollar in the same place as where it began.

Secondly, a dollar that has weakened from a substantially stronger position against world currencies makes U.S. products more affordable overseas. Export demand tends to increase. And corporations with a global presence may see greater profitability.

In sum, financial writers get paid to agonize over the things that might derail investment portfolios. Unfortunately, their words often scare stakeholders and diminish return prospects.

Put another way, if the inflation train was as bad as advertised, stocks would not be performing as well as they are. Nor would stocks be doing so well if participants genuinely believed that interest rates would stay at elevated levels. Likewise, if the dollar was in mortal danger, U.S. stocks would not be setting record highs in July.

This is not to dismiss the reality that any of the above-mentioned challenges could worsen. They could. However, the stock market can usually shake off anxieties and power forward.

The one area that may continue to keep folks on edge? What happens on the date of the new tariff deadline, August 1.

The headlines have been bleak:

• “Trump says 50% tariff on copper imports will begin August 1”

• “Trump threatens 35% tariff on Canadian goods.”

• “Trump announces 30% tariffs on the EU and Mexico, starting Aug. 1.”

Back in April, tariff fears briefly sent U.S. stocks careening toward bear market territory. They recovered in earnest after the White House’s declaration of a 90-day pause. Subsequently, the administration pushed the tariff date back to August 1.

Prior to the 90-day pause, investors struggled with the prospect of a new world trade order. Since the announcement, though, most sense that tariff threats represent a negotiation tactic. Less participants fret about the start of a full-fledged trade war.

Granted, tariff proclamations are likely to continue making the financial markets unpredictable. Nevertheless, there’s equal reason to keep one’s wits, as trade deals and/or modest tariffs are as plausible as any “worst case scenario.”

The good news is that clients of Pacific Park Financial continue benefiting from our systematic approach to risk taking and/or risk reduction. For example, earlier in the year, we reduced our stock allocation prior to the S&P 500 plummeting towards a bearish decline of 20%-plus. Our red dot warning mechanism provided us with the unemotional signal to decrease risk. (See the chart below.)

Similarly, as the 90-day tariff pause served to reassure the investment community, and as stock prices began to recover, we restored allocations to top target levels. Our “green-is-for-go” data point gave us the objective indication to increase risk again. (See the chart above.)

Please contact us if you would like to discuss the particulars of your portfolio. Additionally, Rob and I enjoy chatting about other aspects of your personal finance, including insurance, residential real estate, and retirement.

Warmest Regards,

Gary Gordon, MS, CFP

President