Click Here for a Printer Friendly Version

New Client Portal

You’ve already received a couple of emails from Pacific Park introducing your new Advyzon client portal.

With Advyzon, you can easily view:

• Performance data

• Recent transactions

• Detailed breakdowns of your holdings

The portal also features secure, encrypted document sharing, making file sharing quick and safe. A user-friendly mobile app complements the desktop product.

While the Schwab website remains an excellent resource for real-time account data, Advyzon offers additional tools to:

• Visualize your asset allocation

• Track performance trends

• View all accounts in one place

Advyzon’s client portal is replacing Morningstar’s outdated platform. Please set up your portal promptly to ensure a smooth transition. If you have any questions, please give Rob a call at (949) 600-6294.

Monthly Market Outlook

Stocks showed remarkable resilience throughout 2025, with the S&P 500 on track for its third consecutive year of double-digit gains. Large-cap indices like the S&P 500 remain near their yearly highs despite occasional pullbacks fueled by concerns over AI valuations, a softening labor market, and uncertainty about interest rates.

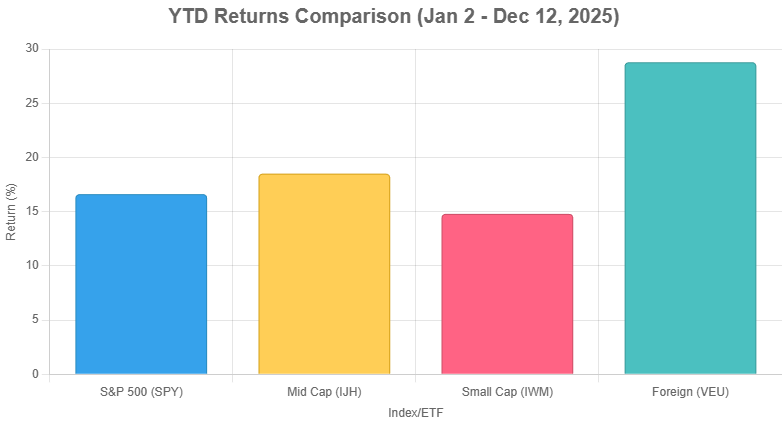

In recent months, mid-cap stocks gained ground relative to large caps, while developed-market foreign stocks also delivered strong year-to-date performance. This broadening of gains suggests investors may be rotating out of concentrated mega-cap technology positions and into smaller companies and international opportunities.

Defensive sectors, such as health care and consumer staples, have recently outperformed technology, signaling investor caution amid cooling employment trends. The labor market weakened notably in late 2025, with non-farm payrolls declining by 105,000 jobs in October (partly due to federal workforce reductions) before a modest rebound of 64,000 in November. The unemployment rate rose to 4.6%, its highest level since September 2021.

Layoff announcements also surged, with Challenger, Gray & Christmas reporting over 1.17 million planned cuts through November. That is the highest annual total since the 2020 pandemic era.

Deterioration in the jobs picture contributed significantly to market volatility in November and December. Additional pressures included trepidation over the Federal Reserve’s policy path. The Fed lowered the federal funds rate to 3.50%-3.75% last week, but officials signaled a more cautious approach to further adjustments in 2026.

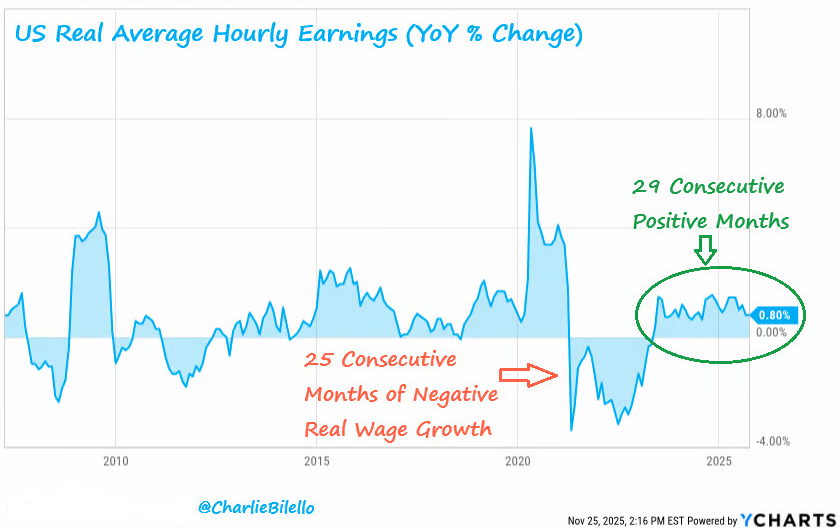

Despite lingering effects from earlier price surges, consumers have benefited from wages outpacing inflation for an extended period. This represents a dramatic shift from the 2021-2022 inflationary environment. (See the shift in average hourly earnings in the chart below.)

Higher borrowing costs continue to weigh on real estate, however. Homeowners with low mortgages (3%-4%) remain reluctant to move (“locked in”), while prospective buyers face limited affordability relief. This has led to subdued housing activity and softer discretionary spending.

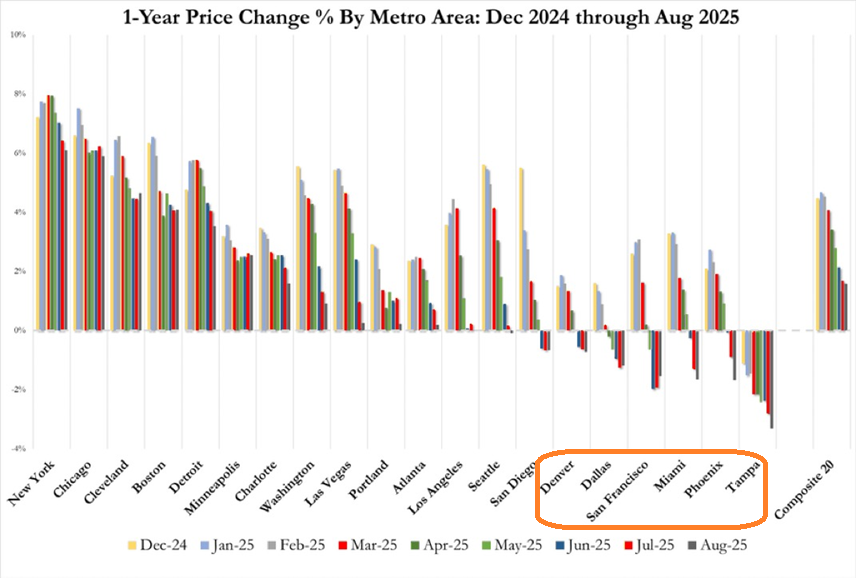

Home prices in several major metros have moderated, with notable year-over-year softening or declines in cities like Tampa, Phoenix, Dallas, Denver, and San Francisco. Absent conventional easing (e.g., rate cuts, stimulus programs, etc.) and unconventional Fed activity (e.g., quantitative easing, asset twists, etc.), home purchases and refinancing could falter in 2026.

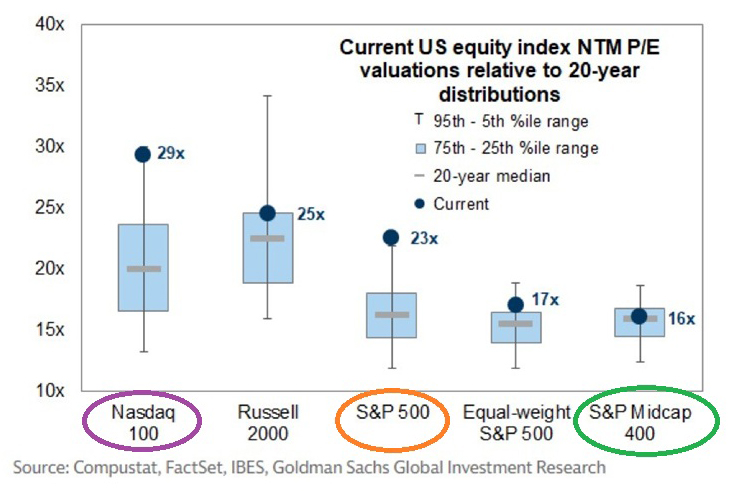

Additionally, concerns persist about a potential AI “bubble,” given stretched valuations in tech-heavy indices like the Nasdaq and S&P 500. By contrast, mid-cap valuations appear more attractive.

The holiday shopping season should receive a lift from the wealth effect of multi-year stock market gains, potentially boosting spending among higher-income households. Lower- and middle-income consumers, though, may remain more constrained amid credit distress.

In summary, late-year volatility stemmed from doubts about AI sustainability, profit-taking, and Federal Reserve policy ambiguity. Still, robust corporate earnings growth, broadening market participation, and accommodative monetary conditions supported overall resilience throughout 2025.

Looking ahead to 2026, the long-term stock market trend remains constructive. The S&P 500’s monthly closing price continues to trade well above its 10-month simple moving average (SMA)—a reliable indicator of underlying market strength. (See the green dots and blue trendline in the chart below.)

As always, we stand ready to raise cash in client accounts should our technical indicators trigger a red warning signal. This disciplined approach has proven highly effective at minimizing drawdowns during major bear markets, including the dot-com bust (2000–2002), the global financial crisis (2008–2009), and the 2022 rate-hike bear.

Please feel free to reach out to us with any questions about your investments. Rob and I would be happy to speak with you.

Warmest Regards,

Gary Gordon, MS, CFP

President