Click Here for a Printer Friendly Version

The U.S. stock market got off to a solid start in January 2026, with the S&P 500 rising about 1.4%. The index briefly surpassed 7,000 before closing the month around 6,939.

In mid-February, stocks became more volatile. The S&P 500 has traded in the 6,800–6,900 range—a modest pullback from recent record highs.

The encouraging development: Market leadership is broadening. Small-cap stocks, tracked by the Russell 2000, surged more than 5% in January. Also, value-oriented shares outside the AI space have outperformed tech-heavy growth stocks.

Some investors are rotating away from “Big Tech” in favor of overlooked sectors (such as energy, materials, and utilities). Others are gravitating toward underappreciated areas like small- and mid-caps.

For example, the Technology Select Sector SPDR Fund (XLK) is down roughly 3% year-to-date. In contrast, last year’s laggards are this year’s leaders, with the Utilities Select Sector SPDR Fund (XLU) up about 8% and the Energy Select Sector SPDR Fund (XLE) up around 20%.

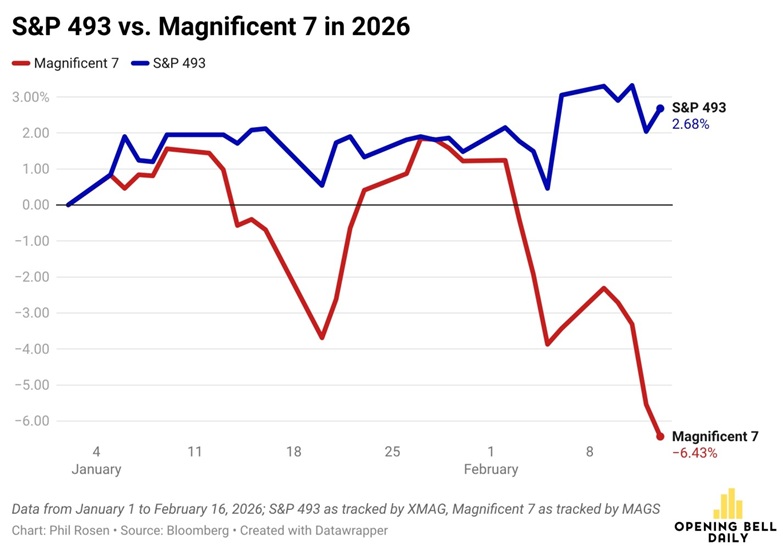

Similarly, the seven largest stocks in the S&P 500 (a.k.a. “The Magnificent 7”) have collectively lost ground in 2026. The other 493 stocks are outperforming.

These shifts might seem concerning for the “AI trade,” but broad-based gains across the market suggest the overall uptrend remains healthy. A well-diversified portfolio can benefit from any continued rotation toward international equities, smaller companies, value stocks, and high-dividend payers.

Turning to fixed income: Bonds delivered strong returns in 2025 amid falling interest rates. In 2026, yields have edged modestly lower, pushing bond prices slightly higher and providing a “win” for bondholders.

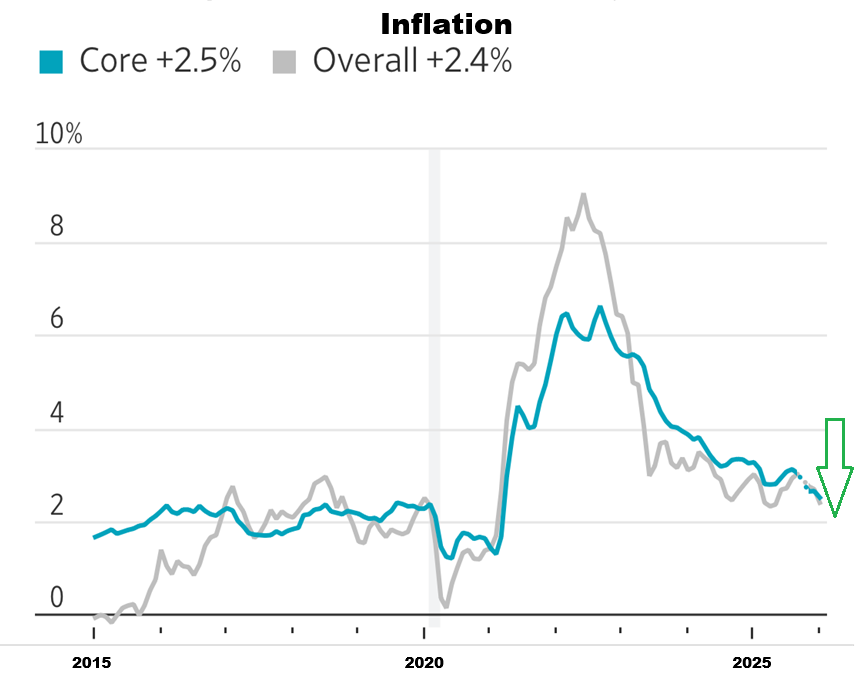

The Federal Reserve held the overnight lending rate steady at 3.50%–3.75% in January. While some expect limited cuts in the future, cooling inflation (CPI at 2.4% year-over-year, down from prior months) supports the case for additional easing.

Overall, bonds are acting like a steady anchor right now. They may not be exciting, but they protect portfolios during stock tantrums.

One note of caution in credit markets: Corporate bond spreads (the extra yield over Treasuries) compressed to multi-decade lows in late January—investment-grade spreads hit a 27-year low, and high-yield spreads an 18-year low.

If geopolitical uncertainty or employment anxiety prompts investors to demand higher compensation for risk, spreads could widen—leading to selling pressure and losses in corporate bonds. U.S. Treasuries would likely benefit from any “risk-off” move.

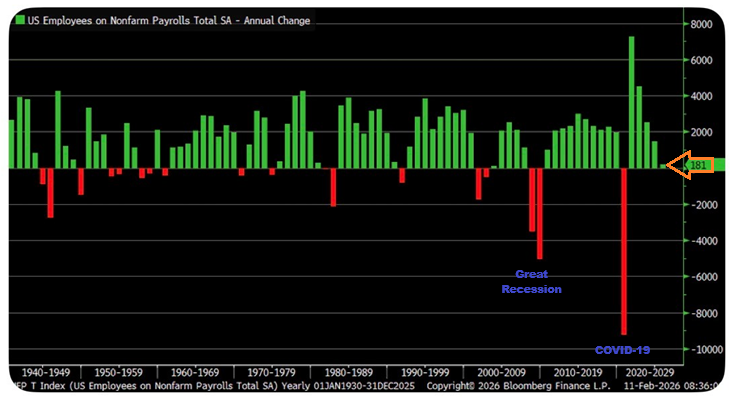

Indeed, investors may be accepting too little extra yield for the added risk. Employment data has shown warning signs for over a year. Most notably, revisions to 2025 nonfarm payroll growth revealed that the U.S. added a mere 181,000 jobs for the full 2025 calendar year (the lowest since 2003, averaging just ~15,000 per month).

Rising employment uncertainty, combined with geopolitical tensions, has driven volatility in precious metals. Gold and silver both hit record highs in January amid global conflicts and safe-haven demand—gold peaked near $5,500/oz and silver around $120/oz. Sharp profit-taking followed, with silver experiencing particularly wild swings (erasing much of its January surge in early February).

Technical Indicators: The Stock Train Keeps Rolling

The S&P 500 closed above its upward-sloping trendline for eight straight months through January (see the green dots and blue trendline in the chart below). The stock trend remains positive.

We are maintaining our target allocations to equities while making modest adjustments to holdings. We continue to diversify by increasing exposure to smaller companies, dividend-paying stocks, international equities, and value-oriented opportunities.

There is little doubt that AI standouts will remain attractive over the long-term. Still, casting a wider net reduces the risks associated with leaving all of one’s eggs in the same basket.

If you’d like to discuss how we’re applying this diversification to your portfolio or any other aspect of your personal finances, please reach out. Rob and I are always happy to meet or chat.

Warmest Regards,

Gary Gordon, MS, CFP

President