Click Here for a Printer Friendly Version

January 2026 has brought sharp market swings, largely from geopolitical tensions. For instance, on January 20, major U.S. stock indexes posted their largest daily declines since October 2025. The S&P 500 fell about 2.1%.

The recent sell-off stemmed from uncertainty regarding a push to acquire Greenland. Markets largely recovered on January 21 and January 22 after Trump ruled out military force as well as removed threats of additional tariffs on several European countries.

Geopolitical headlines and key economic data can spark short-term volatility. In January 2026, we’ve seen the U.S.-led capture of Maduro in Venezuela, civil unrest in Iran, and consistent discussion regarding the White House’s pursuit of Greenland. As a result, stocks may continue trading in wider ranges than might otherwise be anticipated.

Volatile price movement is also occurring in the bond market. Intermediate treasuries have fallen in price (higher yields). Meanwhile, the U.S. dollar is weakening against other currencies.

Stocks: Growth and Volatility

Capital has been shifting away from large-cap growth stocks (heavily weighted in mega-cap tech) toward value, small caps, and international markets. This shift is fueled by expectations of earnings resilience for smaller firms and continued Federal Reserve easing. Small-cap value and growth have been the standout performers, while large-cap growth remains in the red due to valuation concerns and profit-taking.

Extreme concentration in the technology sector has been favorable for investors over the last decade. However, diversification beyond large-cap growth may be one key to investment success in 2026.

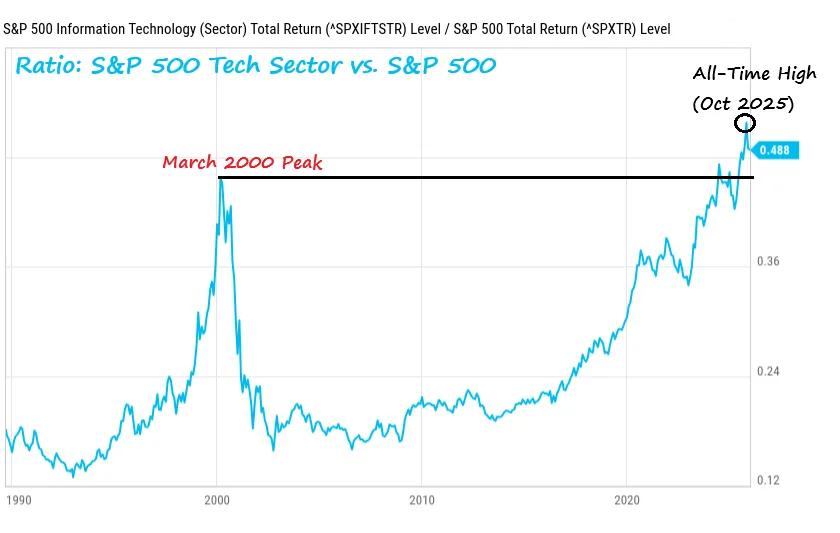

Recently, we noted the tech sector dominates in the S&P 500 stock benchmark – to the tune of 35% exposure. Some analysts suggest that it is closer to 50% when one incorporates certain communication services stocks like Alphabet and some consumer discretionary corporations like Amazon and Tesla.

Regardless of how one dices and slices, a rotation out of tech could hurt the large-cap stock space. Consider the Spider Select Sector Technology ETF (XLK). It has never been more oversubscribed relative to the broader market’s S&P 500 SPDR ETF (SPY). This includes the dot-com internet collapse in 2000.

This doesn’t mean AI investing is over—far from it. Foreign companies and smaller companies could benefit from productivity trends tied to AI.

Clearly, additional diversification in portfolios is warranted. Whereas owning the largest of the large-cap tech behemoths may have been enough in recent years, the combination of Federal Reserve interest rate cuts as well as AI-enhanced productivity should benefit small businesses and foreign companies in the year ahead.

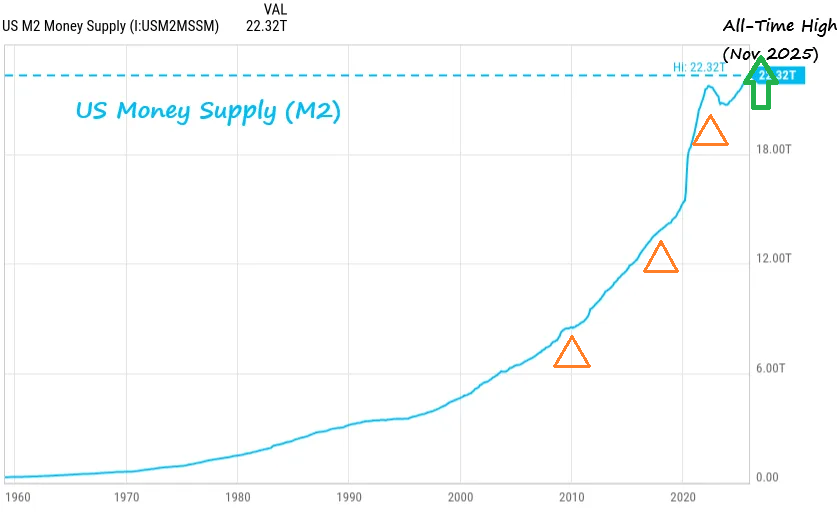

There is an additional tailwind for stocks in 2026: the resumption of money supply growth. Recent history suggests that when the Federal Reserve engages in unconventional stimulus like quantitative easing (“QE”) to grow the money supply, the electronic dollars created find their way into risk assets like stocks.

The opposite is true as well. When the money supply grew less in 2011, 2018 and 2022, stocks had a more difficult time appreciating. The ongoing creation of dollars since Q4 of 2025, though, implies that more dollars are likely to find their way into stocks.

Other issues notwithstanding, the biggest barrier to stock and bond success going forward may be Federal Reserve policy. High borrowing costs for big-ticket items like cars, mortgages, and home furnishings could hinder economic activity.

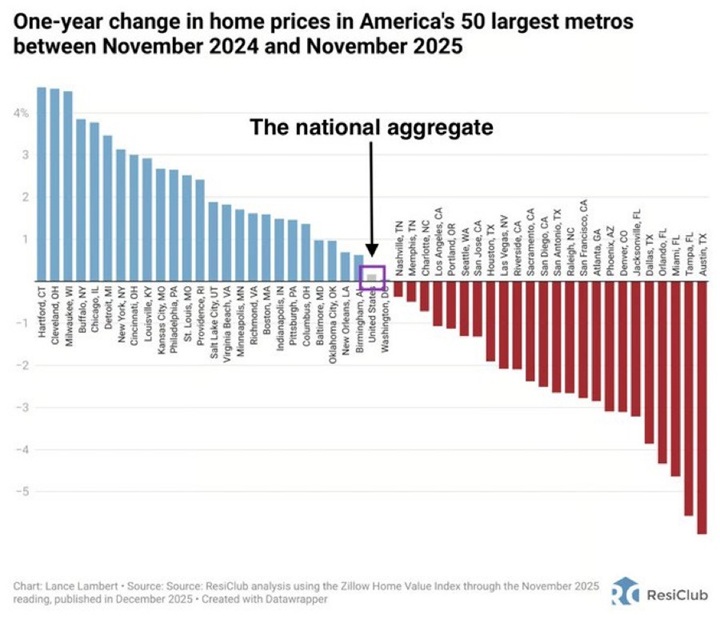

Consider the troubled condition of real estate, particularly residential real estate. Despite a series of cuts to the overnight lending rate, the 10-year yield is no lower than it was 12 months ago. This adversely affects the 30-year fixed mortgage and, by extension, makes it difficult for homebuyers to afford a purchase.

Home sellers are stuck as well:

• Many are unwilling to trade low-rate (3-4%) mortgages for higher ones (6-7%).

• Asking prices haven’t dropped enough to attract buyers.

Bonds: Income and Stability

Turning to bonds, bonds could perform well if the Fed implements additional rate cuts or sells shorter term maturities to buy intermediate-term maturities. Bonds offer reliable income and act as a buffer during stock downturns. Risks include persistent inflation keeping yields elevated or limited cuts.

Bonds continue to serve as a dependable source of income and a counterbalance to equity volatility. More critically, current yields remain attractive relative to historical lows, suggesting that fixed income may be offering compelling opportunity in a lower-rate environment in the years ahead.

Other Assets: Safe Havens and Alternatives

Geopolitical concerns have also pushed capital into perceived safer areas. Precious metals like gold and silver have been popular beneficiaries. Indeed, gold has climbed to near-record levels around $4,900 per ounce amid safe-haven demand, with silver following suit.

Technical Stock Trends

At present, Pacific Park Financial’s indicators continue to flash “green.” Our rules-based system confirms the upward trend remains intact, as shown by the blue trendline.

If the trendline begins sloping downward, we would reduce our allocation to stocks. A downward-sloping trend often signals the potential for further losses.

Similarly, a “red dot” warning appears when the S&P 500’s monthly closing price falls below its long-term trendline. This signal would trigger additional reductions in stock exposure to help safeguard client portfolios from the risk of a severe bear market decline.

Please let us know if you’d like to discuss your portfolio further. We’d be happy to schedule a phone call, Zoom meeting, or in-person visit.

Warmest Regards,

Gary Gordon, MS, CFP

President