Click Here for a Printer Friendly Version

New Client Portal – Coming Soon!

Next week, you’ll receive an email from Pacific Park introducing your new Advyzon client portal.

With Advyzon, you can easily view:

• Performance data

• Recent transactions

• Detailed breakdowns of your holdings

The portal also features secure, encrypted document sharing, making file sharing quick and safe. A user-friendly mobile app complements the desktop product.

While the Schwab website remains an excellent resource for real-time account data, Advyzon offers additional tools to:

• Visualize your asset allocation

• Track performance trends

• View all accounts in one place

Advyzon’s client portal is replacing Morningstar’s outdated platform. Once you receive your introductory e-mail, please set up your portal promptly to ensure a smooth transition.

Monthly Market Outlook

Stocks remain elevated on traditional valuation metrics, supported by expectations of further rate cuts and strong corporate earnings. However, volatility has increased, with the second half of October and early November seeing erratic price swings.

Economic Overview

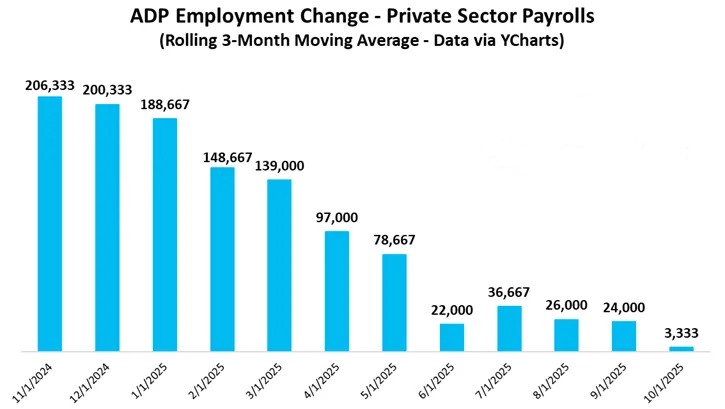

The U.S. economy continues to grow at a modest pace, but labor market weakness is becoming more evident. Layoffs have surged, job growth has slowed markedly, and consumer debt stress is rising.

Private Sector Jobs: Job creation continues to decelerate, with recent data pointing to potential contraction in private payrolls. Additionally, 62% of respondents in a leading sentiment survey expect unemployment to climb—the highest level since 1980.

Layoffs: Major employers are reducing headcount significantly:

• UPS: 50,000 jobs

• Amazon: 14,000 jobs

• Verizon: 15,000 planned cuts

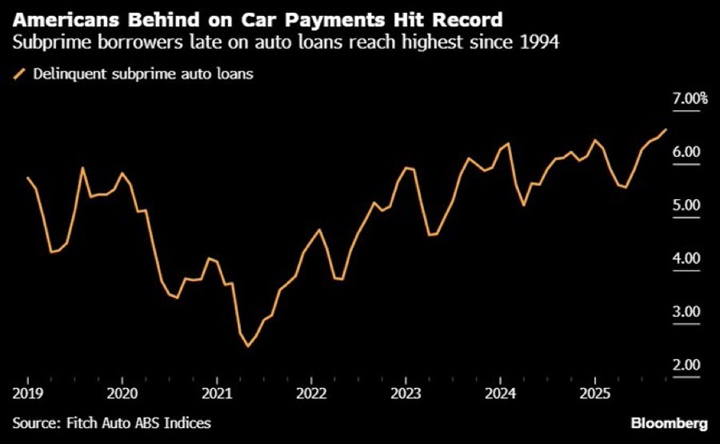

Delinquencies:

• Credit card (90+ days): 12.4% – highest since 2010

• Subprime auto loans (60+ days): 6.6% – worst since 1994

Inflation & Fed Policy: While employment weakness leans deflationary, any persistence in inflation could delay Federal Reserve rate cuts. A slow response by the Fed risks added pressure on housing and consumer spending.

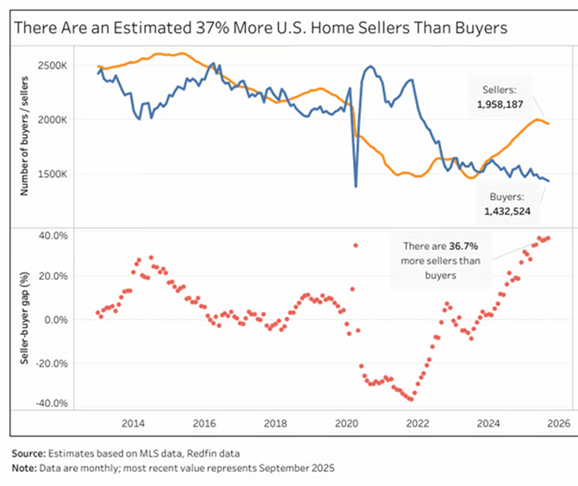

Real Estate Stress:

• Nearly 50% of homeowner income now goes to mortgage, tax, insurance, and interest—a record high.

• Inventory imbalance: 37% more sellers than buyers, signaling affordability challenges for buyers and restlessness for sellers.

Stock Market Implications

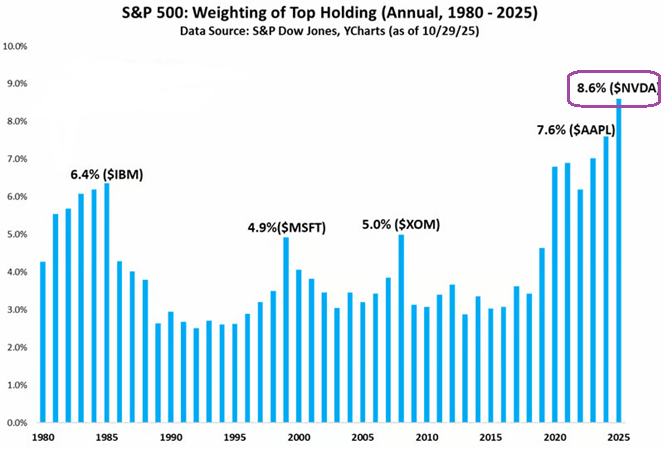

The economic backdrop has created a tale of two markets: AI-driven technology stocks have captured nearly all gains, while most other sectors and smaller stocks lag.

Many clients ask about buying individual AI leaders like Nvidia or Microsoft. However, most index-based portfolios already hold 7–8% in each via ETFs. Adding more increases concentration risk and undermines diversification.

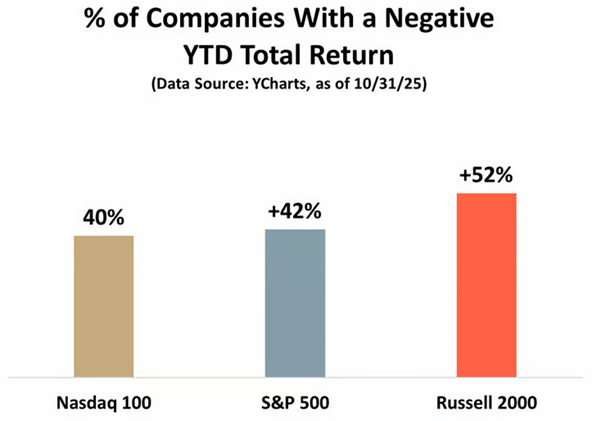

Market concentration:

• The S&P 500’s 14% gain through mid-November is driven by just a few names. The top 10 holdings represent ~40% of the index’s total weight.

• 42% of S&P 500 stocks and 40% of Nasdaq 100 stocks are down in 2025.

• 52% of small-cap stocks are negative year-to-date.

Valuations: Valuations in the AI sector are stretched. Any setback—whether from earnings misses or regulatory scrutiny—could trigger sharp reversals in sentiment.

Technical Outlook

Tech sector rotation has increased intraday volatility. Key levels for the S&P 500:

• Support: 6,700

• Resistance: 6,900

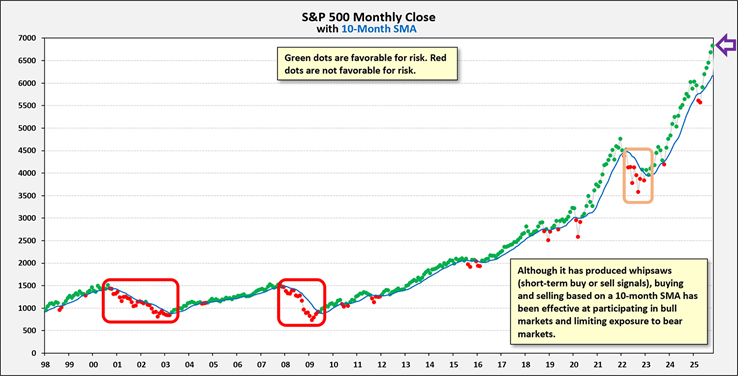

The 10-month simple moving average (SMA), or long-term blue trendline, continues to rise. This implies that stock investing remains favorable. Additionally, our “green-is-for-go” signal (as of 10/31/25) also confirms the uptrend remains intact.

A downward turn in the long-term trendline or a “red dot” warning at month-end would signal elevated bearish risk. In such cases, we would promptly reduce stock exposure to client portfolios.

We welcome questions about your portfolio or any financial topic—investment, retirement, insurance, real estate, or otherwise. Please reach out to us at your convenience.

Warmest Regards,

Gary Gordon, MS, CFP

President