Click Here for a Printer Friendly Version

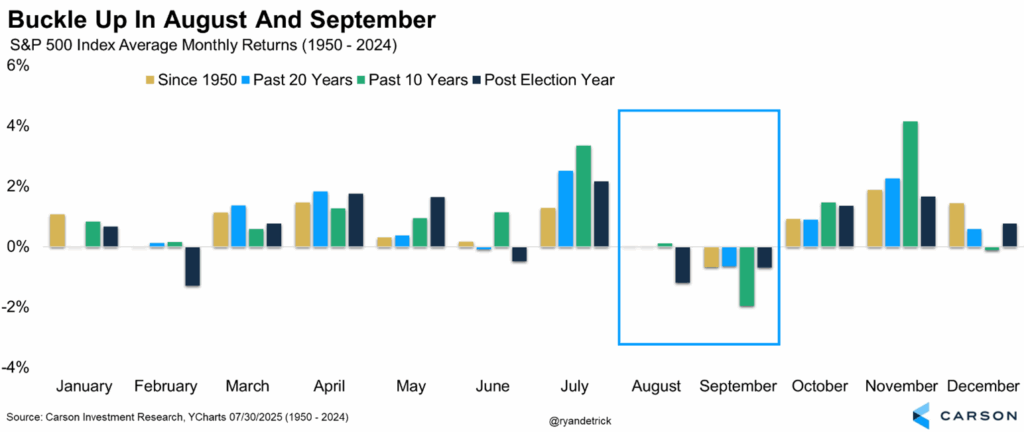

Stocks typically perform poorly in August. The eighth month of the calendar year has experienced an average loss of 0.6% annually since 1990.

Likewise, August historically witnesses a meaningful rise in volatility. The CBOE Volatility Index, or “VIX”, has risen an average of 8.4% over the last 35 years.

Here in 2025, however, performance has been solid, and volatility has been subdued. The S&P 500 continues to notch high after record high. Meanwhile, in a sign that few are fearful, the VIX recently dropped to its lowest level since 2024.

Stock euphoria is a bit startling when one accounts for seasonality patterns. The enthusiasm is even more surprising when one considers the drumbeat of gloomy headlines — tariff troubles, inflation pressures, employment challenges, restrictive interest rates, and recession fears.

Why is the investment community unperturbed by the possibility of plummeting stock prices? The stock market has a long history of dismissing negativity.

For instance, corporations were supposed to make less money because of tariff pressures adversely affecting bottom line profits. Yet, in the most recent quarter, 80% of corporations beat their earnings and revenue expectations.

Similarly, the Consumer Price Index (CPI) was expected to show a substantive uptick in goods-based inflation. It did not. Three-month, six-month, and year-over-year inflation were lower than anticipated. Moreover, the largest components that drove July CPI came from things like airfare, auto insurance, and medical care, which do not genuinely relate to tariff-and-trade policy.

This is not to suggest that tariffs will have no effect on consumer decision making or inflation itself. Nor can one be certain about the profitability of corporations going forward, particularly when producers and importers may need to negotiate tariff-related costs.

What we can extrapolate is that good times are rarely as good as we believe them to be, while bad times are unlikely to be as bad as they are portrayed. Knowing this, Pacific Park Financial allows the markets themselves to tell us when the environment for risk is favorable or unfavorable.

Look at the most recent monthly closing price for the broader stock market. As one can see from the “green data point,” it finished well above the long-term trendline. (See the chart below.)

We also employ the direction, or slope, of the long-term blue trendline. The slope is still moving definitively upward.

In March, the stock market was overwhelmed by tariff ambiguity. Our red dot warning system advocated that we reduce our stock exposure. Essentially, our risk reduction prepared portfolios for the possibility that stocks might fall deeper into a bearish abyss.

Fortunately, the White House changed tactics with its “90-day-tariff pause.” Shortly thereafter, green dots signaled the opportunity to increase risk exposure to stock assets.

Does the current signal mean that the stock market will continue surging ahead? Not necessarily. It implies that the environment for risk-taking is favorable. At least for now.

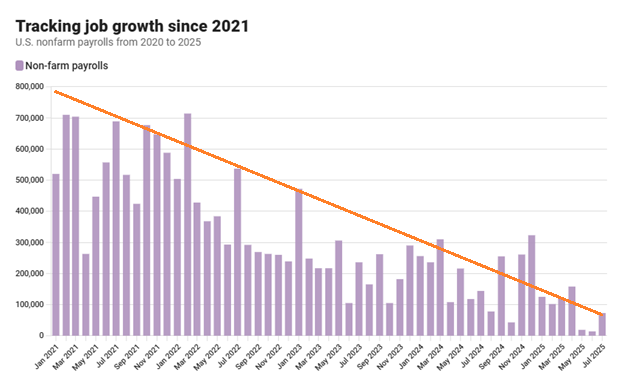

What might cause the next attack of turbulence? One area of concern is the lack of job growth. Although unemployment remains stable, the slowdown in hiring has become increasingly problematic.

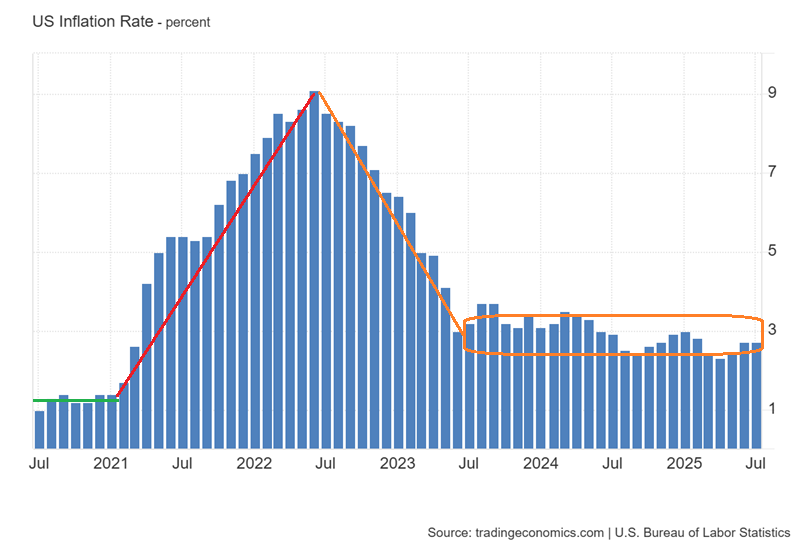

Another area that warrants attention is inflation. On the one hand, inflation has cooled dramatically since the money printing madness that the Federal Reserve engaged in to mitigate the effect of government shutdowns. On the other hand, inflation appears to be settling in at slightly higher levels than what existed before the pandemic began.

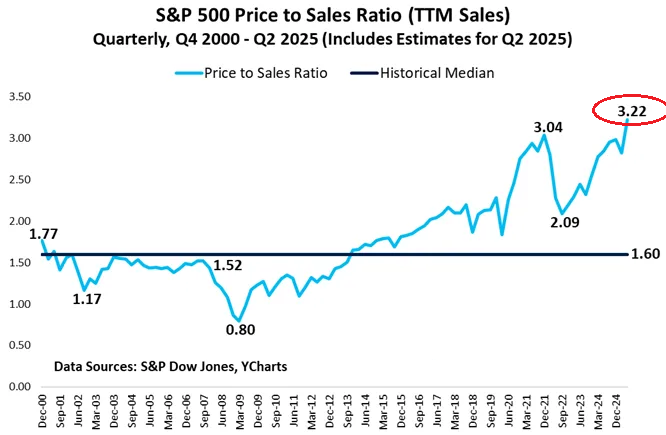

A third area that might set off alarm bells is the exorbitant prices that investors are paying for the privilege of owning U.S. stocks. The large-company barometer, the S&P 500, is trading at a forward price-to-earnings (P/E) ratio of 22.4. That is significantly higher than the 10-year average of 18.4. Meanwhile, at 3.22, the S&P 500 is trading at its highest price-to-sales (P/S) ratio ever.

Reservations notwithstanding, the U.S. economy appears capable of “muddling through.” And that’s a positive for stock-based portfolios.

What’s more, the Federal Reserve is likely to cut interest rates in September as well as December. Rate cutting activity should lead to lower borrowing costs for consumers as well as small businesses.

Would you like to discuss the specifics of your investment positioning? We would love to set up a conversation or meeting.

Warmest Regards,

Gary Gordon, MS, CFP

President